Health Savings Account (HSA) often emerges as a rare opportunity for tax planning. An HSA provides a way to save for medical expenses and offers unique tax benefits that can significantly enhance your overall financial health. In this article, we’ll delve into the nuances of HSA taxes, providing essential tax tips that will help you maximize your savings and minimize your tax liability.

What is an HSA?

A healthcare savings account allows you to set aside money on a pre-tax basis to pay for qualified medical expenses. It was established to provide individuals with High-Deductible Health Plans (HDHPs) a way to pay for current healthcare costs while saving for future medical expenses.

What is the purpose of an HSA Taxes?

The primary purpose of a healthcare savings account is to help offset the costs associated with a high-deductible health plan. However, they also offer significant tax advantages.

Contributions to an HSA are made pre-tax, the interest and earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This tax advantage makes HSAs a powerful tool for healthcare spending and savings.

HSAs also provide flexibility as the funds roll over year after year if you don’t spend them, and the account stays with you regardless of changes in employment or health coverage. This makes an HSA not just a way to cover healthcare costs but also a potential component of long-term savings and investment strategy.

Who Qualifies for an HSA Account?

While Health Savings Accounts (HSAs) offer many advantages, only some can open and contribute to one. To qualify for an HSA, you must meet specific criteria:

High-Deductible Health Plan (HDHP): You must enroll in an HDHP. The criteria for what is considered an HDHP changes yearly, but the plans must meet certain deductibles and out-of-pocket maximums.

No Other Health Coverage: You can’t have any health coverage other than the HDHP. There are exceptions for certain types of insurance such as dental, vision, disability, and long-term care insurance.

Not Enrolled in Medicare: If you receive Medicare benefits, you are no longer eligible to contribute to an HSA. However, if you had an HSA before you enrolled in Medicare, you can still use those funds for qualified medical expenses tax-free.

It’s important to note that while anyone can contribute to your HSA (including your employer or a family member), only the account owner can take the tax deduction for HSA contributions.

Understanding these qualifications can help ensure you fully utilize the benefits of an HSA while staying within IRS guidelines.

HSA Taxes

Contributions to an HSA have significant tax implications. These contributions are pre-tax, meaning they reduce your taxable income. If contributions are made through your employer via payroll deductions, they are made with pre-tax dollars. If you make contributions directly, they are tax-deductible, effectively reducing your taxable income for the year. The result is that you’ll pay less income tax during years when you contribute to an HSA.

HSA IRS Tax Filing

You do need to report HSAs on your tax return. If you made or received contributions during the tax year, you’d fill out IRS Form 8889, “Health Savings Accounts (HSAs).” This form reports all contributions and distributions associated with your HSA.

Part I of the form is where you’ll note your contributions and calculate your deduction. Part II is where you’ll document your distributions and determine if any of the money you used from your HSA is taxable (for instance, if you used it for non-qualified medical expenses). If you over-contribute to your HSA, Part III helps calculate the tax you owe on those excess contributions.

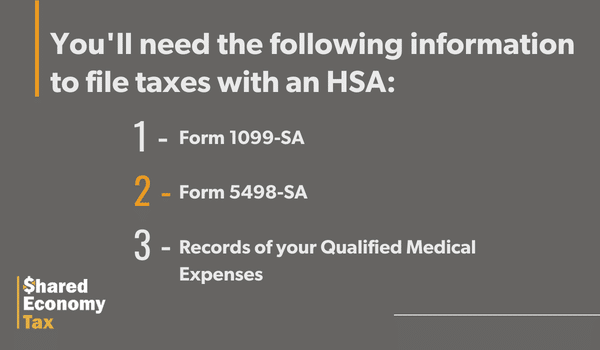

When preparing to file your taxes, you’ll need the following information regarding your HSA:

Form 1099-SA: Your HSA custodian or trustee will provide this information. It shows the total distributions taken from your HSA for the tax year.

Form 5498-SA: Your HSA trustee or custodian will also provide this. This form reports all contributions made to your HSA for the tax year.

Records of your Qualified Medical Expenses: You’ll need documentation (like receipts and invoices) of your medical expenses that justifies the distributions you took from your HSA. These records are important in case of an IRS audit.

Our Top-6 Healthcare Savings Account Tax Tips

There are several tricks to maximize the tax benefits of your HSA.

Track All Medical Expenses

Track all your eligible medical expenses throughout the year. Note that HSA-eligible expenses include expenses not normally considered medical expenses. For example, these non-medical expenses are eligible: insurance, prescription eyeglasses, and over-the-counter medications. You can withdraw an amount equal to your medical expenses from your HSA tax-free.

Rollover Your HSA if You Change Jobs

If you change jobs and your new employer doesn’t have HSA, roll over your balance to an HSA that you open on your own. This allows you to keep your money in an HSA and enjoy tax benefits.

Max Out Your Contributions

The IRS sets the contribution limits for HSAs and changes them each year. For 2023, the contribution limit for individuals is $3,850, and the contribution limit for families is $7,750.

Make Contributions Through Payroll Deductions

If your employer offers an HSA, you can contribute through payroll deduction. This is the easiest way to take advantage of your HSA account since the money comes from your paycheck before taxes come out. Note that some employers also offer to make contributions on your behalf or match your contributions.

Invest Your HSA Funds

Many HSA administrators allow you to invest your HSA funds in various securities. You can invest the money in your HSA in a variety of investment options, such as stocks, bonds, and mutual funds. Though you can keep your HSA funds in cash, investing in other securities can help your money grow over time and give you more money to use for qualified medical expenses.

Don’t Use HSA Funds for Non-Qualified Expenses

Be careful when withdrawing funds from your HSA. If the funds are used for non-qualified expenses, your withdrawals will be subject to income tax and a 20% penalty.

Closing Thoughts on Healthcare Savings Account Taxes

An HSA is a powerful financial tool that combines healthcare planning and tax optimization. Healthcare savings account offer unique tax advantages that can significantly enhance your overall financial well-being, from tax-deductible contributions to tax-free growth and withdrawals for qualified medical expenses.

Understanding how to fully leverage these benefits and comply with IRS guidelines is key to maximizing your savings. Whether planning for imminent healthcare expenses or preparing for future needs, an HSA could be essential to your financial strategy. Remember, every financial situation is unique. So it’s always a good idea to consult with a tax advisor or certified accountant to make the most of your HSA.