If you’re self-employed, a freelancer, an independent contractor, or a gig worker, your financial life looks different from a traditional employee’s. No one withholds taxes for you. No one tracks your expenses. And when it comes time to file, the IRS doesn’t send you a neat summary of what you earned. That’s your job.

The profit and loss statement is the document that makes all of that manageable. It’s not just an accounting formality. For the self-employed, it’s the foundation of your tax filing, your best tool for managing cash flow, and the document you’ll need if you ever apply for a loan, bring on a client who wants to vet your business, or start building a real tax strategy.

Here’s what you need to know.

What is a Profit and Loss Statement?

A profit and loss statement, commonly called a P&L or income statement, is a record of your business revenue and expenses over a specific period of time. Subtract the expenses from the revenue and you have your net income, which is either a profit or a loss.

For self-employed individuals, the P&L isn’t just a management tool. It’s a tax requirement. When you complete Schedule C as a self-employed person, you are in effect creating a year-to-date profit and loss statement for your business. Schedule C, formally titled “Profit or Loss From Business,” is where sole proprietors, single-member LLCs, freelancers, and independent contractors report their income and deductions to the IRS.

In other words: if you file Schedule C, you’re already producing a P&L. The question is whether you’re doing it reactively at tax time, or proactively throughout the year when it can actually help you.

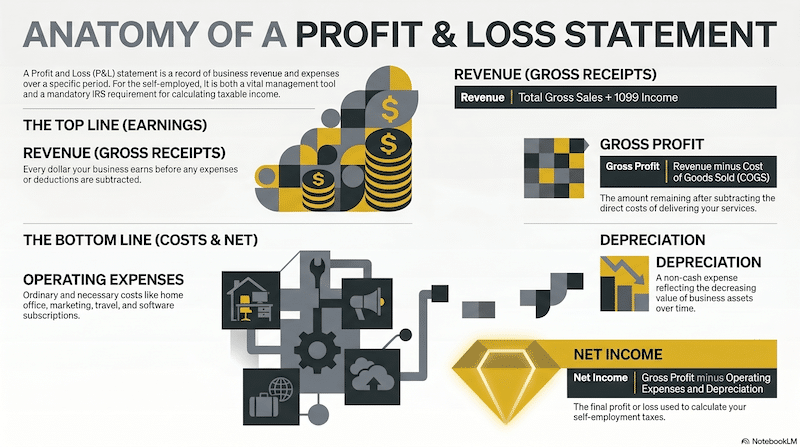

The Core Components

The structure is the same whether you’re a freelance graphic designer, a rideshare driver, or a consultant billing corporate clients.

Revenue (Top Line)

Every dollar your business took in during the period. Start by reporting gross receipts or sales for the year, including amounts reported on 1099 forms issued by clients or others for whom you provided services. If you have multiple income streams, such as project fees plus passive rental income, each should be tracked separately.

Cost of Goods Sold (COGS)

The direct costs tied to delivering your service or product. For many freelancers and consultants, this section is minimal or empty. A copywriter has few direct production costs. A photographer might have equipment costs or contracted editing fees here.

Gross Profit

Revenue minus COGS. This is what you have left before overhead enters the picture.

Operating Expenses

The costs of running the business, including rent, utilities, equipment, accounting, insurance, legal fees, marketing, advertising, and travel. The IRS considers ordinary and necessary operating expenses tax deductible. For self-employed individuals, this is often where the most significant deductions live: home office, software subscriptions, professional development, a dedicated phone line, mileage.

Depreciation

A non-cash expense that reflects the decreasing value of business assets over time. A laptop purchased for your freelance business doesn’t hit your P&L as one lump expense. Depending on how you elect to handle it, it’s either depreciated over several years or fully expensed in the year of purchase.

Net Income (Bottom Line)

What’s left after everything. This is the number the IRS uses to calculate your taxable income, and it’s also the number you’ll pay self-employment tax on.

The Self-Employment Tax Dimension

This is the piece that catches a lot of new freelancers off guard. Self-employed workers are taxed at 15.3 percent of their adjusted net profit, a combination of Social Security at 12.4 percent and Medicare at 2.9 percent. An employee splits this with their employer, each paying half. When you’re self-employed, you cover both sides.

That’s why your net income figure on the P&L isn’t just an accounting outcome. It’s also the base for a significant tax obligation. Lowering your net income through legitimate deductions doesn’t just reduce your income tax. It reduces your self-employment tax too. Every dollar of documented, deductible expense is doing double work.

Contractors, freelancers, gig workers, and others who make more than 400 dollars in profit must pay self-employment tax, which means even modest side income brings real tax responsibility with it.

How Your P&L Connects to Tax Planning

A P&L maintained throughout the year, rather than assembled in a rush before April 15, opens up real planning opportunities.

Timing your expenses

If your net income is running high late in the year and you have planned purchases, accelerating them into the current tax year can reduce what you owe. Equipment, software, professional services, marketing spend. These decisions are hard to make if you don’t know where your net income stands.

Quarterly estimated taxes

Self-employed taxpayers are required to make quarterly estimated payments if they expect to owe taxes when their annual return is filed. Your P&L is what makes those estimates accurate. Without it, you’re guessing and potentially facing underpayment penalties.

Depreciation strategy

This is where it gets meaningful. The One Big Beautiful Bill Act, which became law on July 4, 2025, permanently restores 100% first-year bonus depreciation for eligible assets acquired and placed in service after January 19, 2025.

For freelancers and self-employed professionals investing in equipment, a computer, a camera, a vehicle used for business, this means you can potentially deduct the full cost in the year of purchase rather than spreading it across multiple years. The Section 179 expense limit also increased to 2.5 million dollars for 2025, a threshold far beyond what most individual contractors will spend, meaning virtually any equipment purchase qualifies for full expensing.

The QBI deduction

If your pass-through business earns significant profit, you may be able to deduct up to 20 percent through the Qualified Business Income deduction, assuming you meet all eligibility criteria. Because the deduction phases out at higher income levels and excludes some service industries, working with a qualified advisor is essential to maximize the benefit. Your net income on the P&L is the starting point for calculating whether and how much you qualify for.

If You Also Own a Short-Term Rental Property

A growing number of self-employed and gig-economy workers supplement their income with short-term rental properties on Airbnb, VRBO, or similar platforms. If that describes you, your rental P&L deserves specific attention.

Rental property owners may deduct a range of expenses including mortgage interest, real estate taxes, casualty losses, maintenance, utilities, insurance, and depreciation, all of which reduce the amount of rental income subject to tax.

But there’s a more powerful layer available to active STR owners. The short-term rental tax strategy allows real estate investors to use losses from qualifying short-term rental properties to offset ordinary income, including W-2 and business income. To qualify, the property must meet specific IRS criteria and the owner must materially participate in the rental activity during the tax year.

The restoration of 100 percent bonus depreciation for qualifying property acquired after January 19, 2025 creates a significant planning opportunity for investors using this strategy, especially when timing acquisitions.

For STR owners, maintaining a clean, current P&L for each property isn’t optional. It’s the documentation behind every deduction you claim and the protection you need if the IRS ever asks questions.

Common P&L Mistakes to Avoid

Making a mistake on your P&L can result in costly mistakes, or worse, open you up to IRS penalties. Watch out for these common pitfalls when creating and maintaining your P&L to avoid potential problems.

Treating the bank account as the P&L

Cash in the account tells you what you have. It doesn’t tell you what you earned, what you owe in taxes, or whether you’re actually profitable after expenses. These are different numbers and they require different documents.

Only running it at tax time

A P&L assembled in April is a compliance document. One reviewed monthly is a decision-making tool. The difference between the two is the difference between reacting to your tax bill and planning for it.

Missing legitimate deductions

Self-employed workers can write off a wide variety of business expenses, including vehicle costs, depreciation, home office use, business travel, and professional fees. Freelancers frequently underreport because they don’t have a system for tracking throughout the year. By the time tax season arrives, receipts are missing and expenses are forgotten.

Mixing personal and business spending

This distorts every number on the statement and creates compliance risk if you’re ever audited. A dedicated business checking account and credit card make separation automatic.

Ignoring depreciation

Non-cash expenses don’t feel like expenses, so they get skipped. But depreciation reduces your taxable net income. Missing it means overpaying taxes on income you technically didn’t keep.

Not reconciling against your 1099s

Your P&L revenue total should account for every 1099 you receive, plus any income that wasn’t 1099-reported. Gaps between what clients reported paying you and what you report earning are red flags for the IRS.

How Often to Run Your P&L

Monthly is the standard worth aiming for. Monthly statements let you catch expense trends early, make informed decisions about quarterly estimated payments, and understand the real financial state of your business before the end of the year when your options are still open.

At a minimum, run it quarterly, before each estimated tax payment deadline, so your payments reflect actual income rather than guesswork.

When tracked consistently, a P&L not only shows past business performance but becomes a critical tool for growth planning and securing financing. If you eventually want a loan, a mortgage, or a business credit line, lenders will ask for your P&L. One maintained throughout the year is a very different document from one reconstructed from bank statements the week before your application.

The Bottom Line

For self-employed individuals, the P&L isn’t a bureaucratic formality you hand off to an accountant once a year. It’s the document that tells you whether your business is working, what you owe in taxes, and where your money is actually going.

Maintained consistently, it becomes a planning tool. It shows you when to accelerate expenses, how to time major purchases for maximum tax impact, and whether your quarterly payments are on track. For those who also own rental property, it’s the documentation layer that makes advanced strategies like bonus depreciation and the short-term rental tax strategy defensible.

If you’re a small business owner who wants to step up your tax strategy, look no further than Shared Economy Tax. Our tax pros specialize in helping small businesses, independent contractors, and real estate investors maximize their savings with innovative tax strategies based on the latest IRS regulations. Schedule a a 1-on-1 strategy session with us now to see how much you can save.