According to the recent numbers in a Pew Research study, about 16 million people in the U.S. are self-employed. If you are one of them, you already know that building retirement savings is one of the greatest challenges you face. Fortunately, the SEP IRA offers options for building a retirement for the self-employed, so you can enjoy your retirement years, too.

What Is an SEP IRA?

SEP stands for simplified employee pension. The nature of an SEP IRA is similar to a traditional IRA and follows the same contribution, investment, and rollover rules as other traditional IRAs.

A self-employed pension IRA allows the self-employed to build a retirement savings for themselves and for their employees. The SEP IRA rules allow you to save as much as 10 times the amount of the $6,000 limit allowed by traditional IRAs.

When you compare an SEP vs. Roth IRA, the similarities and differences are the same as between a traditional IRA and Roth. Like a traditional IRA, SEP contributions are taken out pre-tax, and you will pay taxes on them when you begin to draw retirement.

One of the benefits of an SEP IRA is that it allows you to save at an accelerated rate.

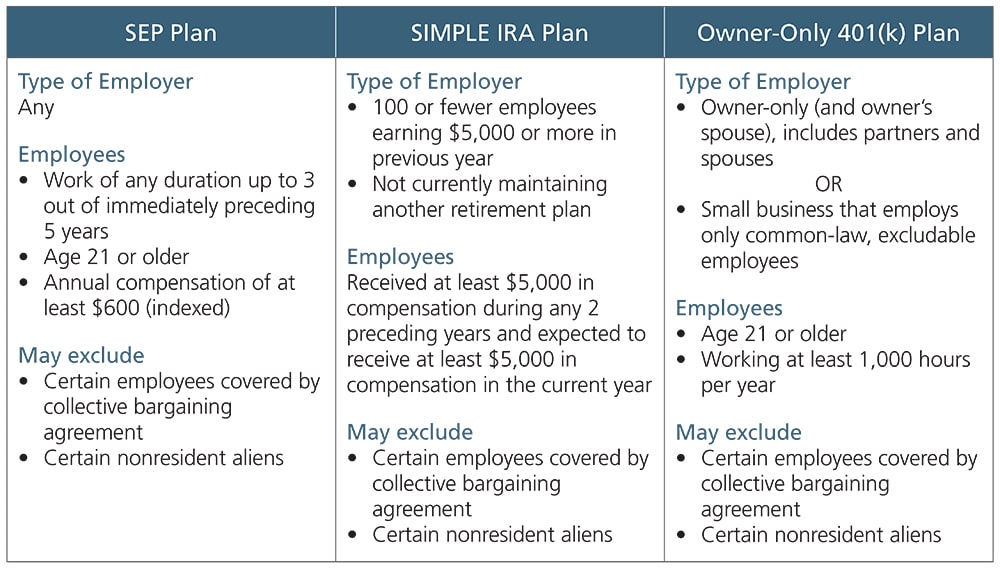

Who Qualifies for an SEP IRA?

To qualify for a SEP IRA, you or your employee must be at least 21 years old and must have worked for the company for three out of the past five years. The employee must have received at least $600 in compensation during the past year.

Another rule that applies to business owners is that you do not have to fund contributions every year, but when you fund your own, you must also fund those of each individual employee at your company.

SEP Contribution and Distribution Rules

Several rules apply to both contributions and distributions under the SEP IRA rules. Here are a few of the most important ones you need to know.

- You will have to pay taxes when distributions are taken.

- Distributions taken before age 59 ½ might incur an early withdrawal penalty.

- You must begin making withdrawals when you reach the age of 70 ½.

- You must contribute in cash and cannot contribute in property.

These are not the only rules, and you can find a complete list on the IRS website. SEP IRA contribution limits 2022 are governed by certain restrictions.

The contribution cannot exceed the lesser of 25% of the employee’s compensation for the year or $61,000. These limits are subject to cost-of-living adjustments.

The SEP IRA contribution deadline is at the time when you file your business taxes, including any extensions.

In most years, it will be April 15. For those who file twice yearly, it will be April 15 and October 15.

The Pros and Cons of SEP IRAs

Here are a few of the pros and cons of SEP IRAs.

Pros

Tax Advantages

When you compare the tax implications of SEP vs SIMPLE IRA vs Self-Employed 401(k), SEP has several advantages.

The first is that for the employer, SEPs for employees are tax-deductible contributions, but they are not deductible for an individual.

You cannot claim SIMPLE IRA contributions, but you can claim them for a solo 401(k) or a Self-Employed IRA. This is one of the main tax advantages of an SEP.

Flexibility for Self-Employed Individuals

An SEP is flexible and easy to set up. All you need to do is to choose an SEP plan, develop a written agreement for allocation, and provide the information to each employee.

Next, you will need to go to the IRS website and set up an SEP IRA account for each employee.

Sizeable Contribution Limits

One of the biggest advantages of an SEP IRA is the large maximum contributions that are allowed. SEP IRA limits are larger than for traditional or Roth IRAs. Limits on SEP IRAs are nearly ten times those of traditional IRAs.

This is good news for those who feel they are behind on their retirement journey.

Cons

Employee Match

For employees, the SEP IRA is a good strategy because your employer must make an equal contribution to your account. They cannot make a larger contribution to their own account than they make to you.

This makes matching contributions to the account enticing. For the employer, it could represent a barrier to starting the plan and maintaining it.

No Catch-Up Contributions

SEP IRAs do not allow “catch-up” contributions, as you can do with a traditional IRA. However, the maximum allowable contributions are up to 10 times higher, so the $1,000 allowable catch-up contribution with a traditional IRA is inconsequential.

SEP IRA vs Self-Employee 401(k)

Another option for building a retirement fund for the self-employed is the Self-Employed 401 (k), which allows you to save up to 100 percent as an employee contribution instead of the 25% limit that applies to SEPs.

A solo 401 (k) will not work for a business that has employees, but an SEP IRA can help small businesses provide retirement benefits to their employees. Another key different is that you can open a solo 401 (k) as a Roth IRA.

When you compare a solo 401k vs SEP IRA, the Solo 401 (k) allows you to build your retirement more quickly.

SEP vs SIMPLE IRA

A SIMPLE IRA allows both the small business owner and employee to make contributions. With an SEP IRA, only the employer makes the contribution, so you cannot take advantage of a matching program.

The SEP has a higher contribution maximum of up to 25% of the employee’s salary, but the SIMPLE IRA is limited to $13,500 with a catch-up limit of $3,000.

Are SEP IRAs the Best Choice for Independent Contractors?

The good news is that if you are self-employed, you now have several options for building a retirement savings. An SEP IRA is a good option for those who prefer a traditional IRA. It is also a good option for small businesses that only have a few employees.

For those who are a solopreneur with no employees, a solo 401 (k) might be your best option because the contribution levels are higher.

The bottom line is that you need to carefully examine the tax implications of each option and decide which is right for you.

More Self-Employed Tax Strategies

Shared Economy Tax specialize in taxes for freelancers, Airbnb hosts, and other self-employed earners. Set up a one-on-one strategy session with one of our tax experts today to see how much you can save.

Don’t forget to sign up for our tax tips newsletter below for even more money-saving tax tips.