When you sell a profitable investment, whether it’s real estate, stock, or another asset, a capital gains tax bill often follows. The size of that bill depends on what you sold, how long you held it, and, most importantly, whether you had a strategy in place before the sale.

The good news is that the tax code offers several legitimate and well-established tools to defer or reduce capital gains taxes. The better news is that recent legislation has updated and in some cases significantly improved some of those tools. This guide covers the key strategies, how they work, and what’s changed for 2025 and 2026.

What Are Capital Gains?

Capital gains are the profits you realize from selling an asset for more than you originally paid for it. They can be generated from a wide range of assets, including:

- Stocks and privately held business equity

- Bonds sold in the open market

- Real estate, including investment properties and personal residences

- Precious metals such as gold and silver

- Cryptocurrency, which the IRS treats as property and requires you to disclose on your return

- Collectibles such as art, coins, or stamps

If the sale price exceeds what you originally paid, the difference is a capital gain, and the IRS will want its share unless you take steps to defer or exclude it.

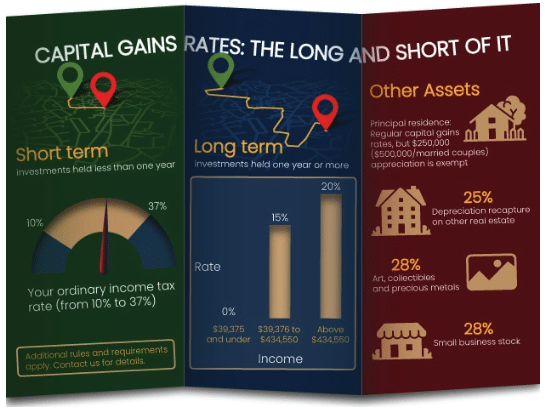

Long-Term vs Short-Term Capital Gains

How your gains are taxed depends heavily on how long you held the asset before selling. This distinction is one of the most impactful variables in investment tax planning.

Long-term capital gains apply to assets held for more than one year. These are taxed at preferential rates of 0, 15, or 20 percent depending on your total taxable income. For most investors, simply holding an asset past the one-year mark produces a meaningful reduction in tax liability.

Short-term capital gains apply to assets held for one year or less. These are taxed at ordinary income rates, which can reach as high as 37 percent. The difference between a short-term and long-term rate on a significant gain can amount to tens of thousands of dollars.

Capital gains may also be subject to the 3.8 percent Net Investment Income Tax for higher-income filers, which adds another layer of planning consideration.

From https://udcpas.com/2019/12/09/infographic-capital-gains-tax-can-take-a-bite-out-of-your-investments/

Key Terms to Understand Before You Plan

Before evaluating strategies, it helps to be clear on a few foundational terms:

Basis is what the asset cost you. It’s subtracted from the sale price to determine your taxable gain. Basis can be increased by capital improvements or adjusted for depreciation.

Sales proceeds are the total amount received from the sale before adjustments.

Date acquired or placed in service determines your holding period. For stock, ownership begins on the acquisition date. For rental property, it begins on the date the property is first available for rent.

Cost of sale includes attorney fees, closing costs, commissions, and other transaction expenses. These reduce your taxable gain and should be documented carefully.

Strategies for Deferring Capital Gains Taxes

The following strategies allow you to delay when capital gains taxes are due, often by reinvesting proceeds into qualifying assets rather than receiving cash.

1031 Exchange

A 1031 exchange allows real estate investors to defer capital gains taxes on the sale of an investment property by reinvesting the proceeds into another like-kind property. Like-kind means the same category of property: a rental property exchanged for another rental property, or a commercial building for another commercial building. It does not apply to primary residences, vehicles, or personal property.

The core rules remain straightforward:

- You must identify a replacement property within 45 days of closing the sale.

- You must complete the purchase within 180 days.

- Proceeds must flow through a qualified intermediary, a third party who holds the funds in escrow. You cannot receive or control the money yourself without triggering immediate tax liability.

A 1031 exchange defers taxes, it doesn’t eliminate them. When you eventually sell the replacement property, the deferred gain comes due, unless you execute another exchange. This is why experienced investors treat the 1031 as a long-term accumulation strategy rather than a one-time move.

One particularly powerful application: if you continue 1031-ing throughout your lifetime and the property passes to your heirs, they receive a step-up in basis to the fair market value at the time of inheritance. This means the deferred gain you’ve been carrying may never be taxed at all. It’s one of the most effective wealth transfer strategies available to real estate investors.

Opportunity Zone Investments (OZ 1.0 and OZ 2.0)

Opportunity Zones were created by the 2017 Tax Cuts and Jobs Act to encourage investment in economically distressed communities. The core mechanics: reinvest capital gains into a Qualified Opportunity Fund (QOF) within 180 days of a sale, and the tax on those original gains is deferred. If you hold the QOF investment for at least 10 years, any appreciation on the new investment itself may be permanently excluded from tax.

What’s changed in 2025 and 2026: This is an area where investors need to update their understanding, because the rules have shifted significantly.

Under the original Opportunity Zone program (OZ 1.0), the deferred gain had to be recognized by December 31, 2026, at the latest. That deadline still applies to existing OZ 1.0 investments made under the old rules. Investors who are currently holding OZ 1.0 fund positions should be actively planning around that recognition event now.

The One Big Beautiful Bill Act introduced OZ 2.0, which makes the Opportunity Zone program permanent and removes the fixed 2026 recognition date for new investments. Under OZ 2.0, the deferral period is based on a rolling five-year window from the date of investment rather than a fixed calendar deadline. However, OZ 2.0 incentives only apply to investments made on or after January 1, 2027.

This creates a planning opportunity known as the “bridge strategy.” An investor can defer a 2025 capital gain into an OZ 1.0 fund now, and later sell that position before the 2026 recognition deadline. The sale triggers a fresh 180-day window to reinvest into a new QOF, potentially positioning the investor to take advantage of the enhanced OZ 2.0 benefits once they take effect. This is a nuanced strategy that requires careful coordination with a tax advisor, but the mechanics are sound.

Section 1202 Exclusion: Qualified Small Business Stock

Section 1202 of the Internal Revenue Code allows investors in certain small businesses to exclude up to 100 percent of their capital gains from federal taxes. This is primarily a strategy for early-stage company investors and startup founders, not real estate.

To qualify:

- The stock must have been held for at least five years.

- The issuing company must be a C corporation with gross assets of $50 million or less at the time the stock was issued.

- The company cannot operate in certain excluded industries, including legal, accounting, consulting, and financial services.

For stock purchased after September 27, 2010, the federal exclusion is 100 percent. Note that state taxes may still apply, as not all states conform to the federal exclusion. If you are an investor in a qualifying startup or small business, this provision is worth examining carefully before any liquidity event.

Additional Tax Reduction Strategies

Beyond the primary deferral tools above, these strategies can meaningfully reduce your overall capital gains exposure.

Installment Sales

If you sell real estate or another large asset and don’t need all the proceeds immediately, an installment sale allows you to spread the gain recognition over multiple years. Rather than reporting the entire taxable gain in the year of sale, you report income proportionally as you receive payments.

This strategy works well when you expect to be in a lower tax bracket in future years, or when spreading the gain prevents it from pushing you into a higher bracket or triggering the Net Investment Income Tax in a single year. It’s governed by IRS Publication 537 and involves meaningful complexity, particularly around interest calculations and basis allocation. Working with a tax attorney or CPA before structuring the sale is essential.

Tax-Loss Harvesting

If you have realized capital gains in a given year, selling other investments at a loss can offset those gains dollar for dollar. This practice is commonly referred to as tax loss harvesting.

Short-term losses offset short-term gains first, and long-term losses offset long-term gains. After netting gains and losses, up to $3,000 in remaining net losses can be deducted against ordinary income annually, with unused losses carried forward to future years.

For real estate investors, understanding how capital losses on investment properties work is particularly important, since the rules differ from how losses on stocks and securities are treated.

One important constraint applies primarily to securities: the wash-sale rule prohibits repurchasing the same or substantially identical security within 30 days before or after the sale. Violating this rule disallows the loss deduction.

Primary Residence Exclusion

Under Section 121 of the Internal Revenue Code, homeowners can exclude up to $250,000 in capital gains from the sale of a primary residence, or up to $500,000 for married couples filing jointly. To qualify, you must have owned the home and used it as your primary residence for at least two of the five years prior to the sale.

This exclusion does not apply to second homes or investment properties in general. However, if you lived in a rental property as your primary residence within the prior three years, you may still be eligible for a partial exclusion. This is an underutilized planning opportunity for investors who have transitioned a property between personal use and rental use.

Depreciation as a Complementary Strategy

For real estate investors, depreciation isn’t just an accounting entry. It’s one of the most powerful tools available for reducing taxable income year over year, and it interacts directly with your capital gains planning.

Cost segregation is a strategy that accelerates depreciation by breaking a property into its individual components and assigning each one a shorter useful life. Rather than depreciating the entire structure over 27.5 or 39 years, cost segregation allows you to depreciate fixtures, flooring, appliances, landscaping, and other components over 5, 7, or 15 years instead.

For STR investors and Airbnb hosts in particular, a cost segregation study can generate significant paper losses in the early years of ownership that offset rental income and, in some cases, other income sources.

The One Big Beautiful Bill Act permanently restored 100 percent first-year bonus depreciation for qualifying property placed in service after January 19, 2025, reversing the phase-down that had reduced the rate to 40 percent. This change significantly increases the value of cost segregation studies completed in conjunction with new property acquisitions.

One important consideration: depreciation reduces your cost basis, which means higher gain recognition when you sell. This is why Section 1245 and Section 1250 depreciation recapture rules matter. Recaptured depreciation is taxed at a higher rate than long-term capital gains, and the interaction between depreciation strategy and exit planning is a key area where working with a tax professional pays off.

Why Timing and Planning Matter

Capital gains tax strategy is not something you implement after the fact. The most powerful tools, 1031 exchanges, Opportunity Zones, installment sales, all require decisions made before or at the time of the transaction. A sale structured without a plan in place leaves very few options afterward.

The current environment rewards proactive planning. The OBBBA has introduced both new opportunities and new deadlines, particularly around Opportunity Zones, and the window between now and the end of 2026 is meaningful for investors with existing OZ positions or significant unrealized gains.

It’s also worth noting that capital gains interact with other parts of your tax picture in ways that aren’t always obvious. A large gain can push you above thresholds that trigger the Net Investment Income Tax, reduce eligibility for certain deductions, or affect your quarterly estimated tax obligations.

Investors who understand how to avoid underpayment penalties by planning their estimated payments around anticipated gains can avoid a costly and frustrating surprise at filing time.

Work With a Tax Professional Who Understands Investors

These strategies each come with specific qualification requirements, deadlines, and interaction effects that can significantly change the outcome if misapplied. A missed 45-day identification window on a 1031 exchange, an OZ investment that doesn’t meet reinvestment timing, or an installment sale structured incorrectly can trigger the very tax bill you were trying to avoid.

Shared Economy Tax specializes in tax strategy for real estate investors, business owners, and self-employed professionals. If you have a pending sale or significant unrealized gains, schedule a free one-on-one strategy session with our team to find out which approach makes the most sense for your situation.