Entrepreneurs look for legitimate ways to save money and improve their cash flows. Lowering the tax burden is one such way but take caution concerning a preparer. Swindlers run scams promising outsized refunds yet they lack any credentials that would affirm knowledge and experience in this area. Airbnb owners are subject to such deceit, especially as they look for tax advantages relative to mortgages. This article explains the mortgage process that a legitimate preparer should know.

Understanding Airbnb Mortgages

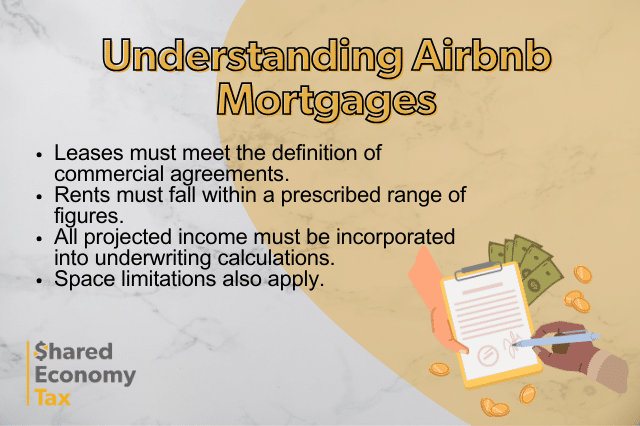

While there are no loan products named “Airbnb Mortgage,” landlords have a number of commercial mortgages available for investment properties. The idea behind Airbnb is that such properties fill two needs: renters’ desire for affordable lodging and owners’ desire for reliable income streams. Mortgagors, in turn, measure demand at rental rates that will cover the monthly payments on the property loan. Of course, property owners offer rates cheaper than local hotels to make their assets more attractive to those looking for short-term accommodations. Credit issued against income properties generally requires a higher interest rate than a loan for, say, a primary residence. So, the landlord/borrower must fix prices to both debt service the mortgage and provide a modest profit after all input expenses are paid. When approving or denying applications for credit on short-term rental properties, lenders adhere to guidelines from Fannie Mae, the government chartered investor in home mortgages. These include:

Preparing Your Finances for an Airbnb Mortgage

Commercial mortgages are underwritten to confirm that the revenue from the real estate is sufficient to cover the monthly payments. Therefore, loan applicants do well to prepare detailed rent rolls for refinances, backed up by active leases. With purchases, however, prospective borrowers must use projected income so they should provide some evidence of market analysis for the subject property and a record of successful property management.

Some of this data is in a commercial appraisal that takes an income approach.

Those acquiring new property must also be creditworthy and demonstrate competence in terms of income generation through real estate. As with any mortgage, a strong credit score, documentation of assets and other sources of revenue help lenders evaluate the risk level of each applicant. New investors are better off if they work for an employer and demonstrate longevity on the job. Veteran investors, meanwhile, should show a portfolio of real estate assets along with proof of their financial performance. Again, it is all about making the extension of credit less hazardous for the bank.

Exploring Mortgage Options for Airbnb Hosts

Choosing among an array of loan products makes all the difference with a property’s cash flow and a borrower’s finances. Commercial real estate mortgages differ from their residential counterparts in that 1) They are issued to business entities as opposed to individuals; 2) their terms are usually under 20 years; 3) and their equity (ownership) demands are higher as expressed by lower loan-to-value ratios. In some cases, however, states and cities allow primary residences to have Airbnb units on the property. In such instances, borrowers can get a conventional residential mortgage even though the home also serves as an income stream. Plus, residences have access to government-backed (FHA, VA e.g.) credit that is easier to obtain. Home equity loans and second mortgages are also open to owner-occupants.

With this option on the shelf, what other loan products work for these short-term rental structures? Generally, real estate loans for non-owner occupied sites are subject to the low LTV and shorter loan terms that typify commercial and investment mortgages. In any event, houses reserved strictly for investment have other avenues available for financing. Private mortgages, for example, are loans offered by other investors — either individuals or enterprises — and the qualification standards are more subjective than conventional or government-guaranteed loans. Self-employed and other borrowers appreciate the quickness and ease in which private loans are approved. At the same time, the interest rates are high, the terms can be quite short and borrowers receive few of the consumer protections that their peers get from traditional banks and finance companies.

Navigating the Application Process

1. Thoroughly familiarize yourself with the loan eligibility requirements.

2. Apply according to lender specifications

3. Obtain a pre-approval before deciding on a property or properties. A pre-qualification is a cursory evaluation based on stated information. A pre-approval, on the other hand, is based on a largely underwritten loan application.

4. Investigate properties based on the pre-approved loan amount and on what the estimated return on investment would be after operating costs. Short-term rentals are sometimes viewed as riskier from a banks viewpoint.

Leveraging Airbnb Income for Loan Qualification

The best evidence to back up your claims of projected income is a record of profits from short-term rentals. This makes real the potential of the subject property — when the owner brings a strong track record. A large asset base and substantial downpayment likewise gives confidence to underwriters.

Managing Multiple Airbnb Mortgages

Carrying mortgages on several Airbnb properties is theoretically no trickier than managing one. However, financial institutions may insist on higher equity on each successive piece of collateral. Additionally, a higher rate might apply and a larger asset base may likewise be mandatory for the lender’s comfort. Having the financial flexibility to meet these criteria — and the income to offset them — is best for those who wish to finance more than one property. Refinancing higher interest mortgages after the season helps to lower input costs.

Assemble a Team of Professionals

Loan recipients are exposed to financial, legal and commercial hazards as they draw revenue from Airbnb locations. Fielding the right professionals — realtors, attorneys and accountants, e.g. — is essential for limiting that exposure.

Conclusion

Airbnb owners operate investment properties and are subject to the unique mandates of commercial mortgages. prospective hosts should be certain to have sufficient financial resources to meet their standards and then some. Get started now with a one-on-one strategy session with one of our tax pros.